India’s ratio of trade covered by credit insurance to GDP is around 5% as against 10% in China and over 20% in some of major European economies

If policymakers really want to strengthen and stimulate India’s exports, they have to liberalise the credit insurance sector again. One firm’s misdeeds cannot translate into collective punishment. Is that too big an ask?

The Dollar Business Bureau | @TheDollarBiz

Rajeev Mehrotra, a candle manufacturer and exporter based out of Dehradun (the capital city of the state of Uttarakhand), has been supplying high-quality scented candles and other wax products to countries like US and UK for years now. His well-developed network of trusted agents and partners in these two countries have been doing it all for him – from identifying customers to realising sale proceeds from them once the products have been delivered. And he has never faced any problem so far. But he is not satisfied with the way he is running his business. He wants to expand his business and export to other countries where wax products, like his company manufactures, are in high demand. It’s not that he has not been receiving export inquires or orders from other countries, it’s just that he has been hesitant in accepting them as they are from a country where he has no trusted partner or an agent. But this is not how he wants to run his business forever. “I want to grow my business. For that I need to supply to other countries. I have been receiving sales inquiries, even orders, from importers from countries like Israel, Egypt etc., but I am a little sceptical about them. I don’t want to be in a situation where I supply to them and don’t realise the sale proceeds. But then, I want to expand my business. However, I don’t know a way out this awkward situation,” he tells The Dollar Business.

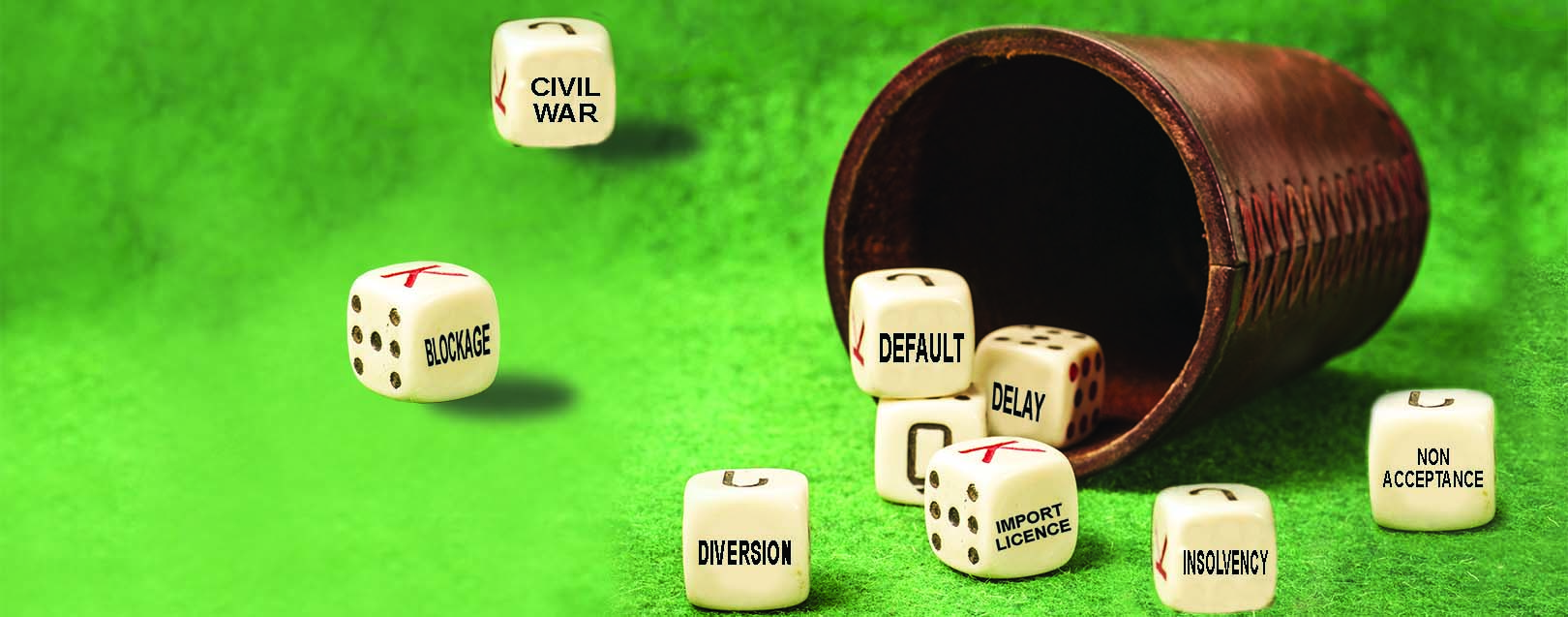

Interestingly, Mehrotra is not the only one facing the predicament. There are many exporters, across the country, who have been letting go such opportunities just because they didn’t know someone who could cover their back in the land unknown. And not just small and mid-sized exporters, even the bigger fishes of the pond, at times, find it difficult to respect the payment terms demanded by buyers. In fact, receivables from exports are vulnerable to risks even at the best of times. A coup or an outbreak of civil war in the destination country, sudden restriction on import of certain goods by the importing nation, protracted defaults, commercial risk of insolvency of a foreign buyer etc., are some of the many risks that may delay payment for goods exported or even lead to defaults at times. So what do an exporter do if he wants to expand his overseas business without fear of loss? That’s where the ‘Export Credit Insurance’ comes to an exporters help – an insurance cover that can watch an exporters back while he is busy expanding his business overseas. The scheme Consider another example. A fast-growing leather manufacturer and exporter was shaken when his biggest customer, a multi-million dollar leather retailer, declared insolvency. The sudden closure caused millions of rupees in receivable losses across the globe, and left this leather exporter alone facing Rs.7.5 million in exposure. The catastrophic loss crippled the leather exporter for a long time and it took them more than 3 years to come back to its former state. This won’t have been the case if that leather exporter had insured himself against that credit risk. Certainly, credit risks can jeopardize the continued existence of a company. While late payments can slow down growth and reduce profitability (as fewer financial means are available to make necessary investments), non-payment can even lead to bankruptcy at times. And to ward off these threats there is what we call export credit insurance. It’s an insurance policy and risk management product designed to protect exporters from the consequences of such payment risks, both commercial and political (a good example of political risk was when the Russian government declared a moratorium on all foreign debt in 1998, including trade debt, as a measure to keep hard currencies in the country during its financial crisis. It had crippled a lot of companies), and to enable them to expand their overseas business without fear of loss. Export credit insurance usually covers a portfolio of buyers and pays an agreed percentage of an invoice or receivable that remains unpaid as a result of protracted default, insolvency or bankruptcy. Trade credit insurance is purchased by business entities to insure their accounts receivable from loss due to the non-payment of valid debt by their debtors. It can also be expanded to cover losses resulting from political risks such as currency inconvertibility; war and civil disturbance; confiscation, expropriation and nationalisation and as the one discussed above. Credit insurance policies, which are currently offered in India, can be broadly grouped into three types – Whole Turnover Policy (covers all customers of the policyholder), Key Account Policy (covers the policyholder’s largest customers) and Single-buyer Policy (covers a single buyer of the policyholder). Further, export credit insurance generally covers short-term risks for periods not exceeding 365 days, and normally for periods of between 90 and 180 days. Monopolistic market Interestingly, as per insurance regulations, only Export Credit Guarantee Corporation of India Ltd. (ECGC), owned by Government of India, is permitted to sell all kinds of export credit policies. The rest are only allowed to sell the Whole Turnover policy. Insurance Regulatory and Development Authority (IRDA) had banned all forms of credit insurance, except through Export Credit Guarantee Corporation of India Ltd (ECGC), in 2010 (though three months later it allowed companies to provide limited trade credit protection) in the wake of large defaults on credit insurance policies issued by some state-owned insurers. As per the current guidelines, credit insurance policies also cannot be assigned to banks. In other words, a seller cannot realise the proceeds of sale from a bank using the credit insurance policy as a security. Although the regulator has re-allowed credit insurance, the restrictions means that needs of several sellers remain unfulfilled. This has adversely impacted the export credit insurance market in India. Agrees Kunal Mehta, a Delhi based Export-Import Consultant, as he tells The Dollar Business, “The regulation has larger implications for the economy than is being probably understood. Both domestic and international trade is a major driver and contributor for the growth in the national GDP. Export credit insurance has proved to be an enabler of trade according to studies conducted by WTO as well as the Centre for European Policy Studies. Restricting it will only have adverse effect on India’s widening current account deficit.” The need of the hour This is certainly a major concern for a country like India that has been perennially running a merchandise trade deficit of over $100 billion for each of the last five years. If India really wants to strengthen and stimulate its export sector, it certainly needs to open up the export credit insurance sector once again. Relying on just one player – ECGC – will only deteriorate the situation further. Interestingly, ECGC provided most of the coverage, accounting for almost 100% of total premium paid for short-term trade credit insurance, in FY2014. And that has been the trend since IRDA’s ban in 2010. But this can’t go on forever.

The size of the credit insurance market in India is still small when compared to its global peers. In fact, India’s ratio of trade covered by credit insurance to GDP is around 5% as against 10% in China and over 20% in some of major European economies. Hence, the need of the hour is a flexible credit insurance regime to aid commerce and trade. It will not only enhance the competitiveness of Indian multinationals, but will also encourage small and medium enterprises (SMEs) to take up exports. “Instead of restricting the product, the regulator should have taken strict action against those who did not follow prudent risk management practices,” says Mehta. It would have certainly been better if the regulator would have ensured that the principles of insurance and reinsurance are applied on credit insurance in a similar manner the way they are being applied on all other products. Other factors hampering the growth of export credit insurance in India, including lack of product awareness, self-insurance (maintaining sufficient bad debt reserves), cost constraints and limited distribution channels in marketing this specialty product, also needs to be addressed on an urgent basis. How soon? Well, as soon as our policymakers wake up from their slumber!

Copyright @2026 The Dollar Business. All rights reserved.