GJF recommends gold import duty cuts, exclusion of jewellery from FTAs

India exported gold jewellery worth around $8.1 billion in FY2013-14, down 38% from $13 billion in FY2012-13

India exported gold jewellery worth around $8.1 billion in FY2013-14, down 38% from $13 billion in FY2012-13The All India Gems and Jewellery Trade Federation (GJF), a trade body for the promotion and growth of trade in gems and jewellery across India, has urged the government to develop a comprehensive gold policy to make India a global jewellery hub as a part of Prime Minister Narendra Modi’s “Make in India” initiative. Among its recommendations for Union Budget 2015-16, GJF said that considering that crude oil prices are expected to be low, the government should reduce the import duty on gold from 10% to around 2% to strengthen the domestic gold industry and prevent smuggling of gold into the country. According to a GJEPC report, Haresh Soni, Chairman, GJF, said that the government must also ensure that the difference between the import duty between the raw materials (gold and silver) and finished jewellery must be maintained at least 10% for gold and 15% for silver.

Source - Ministry of Commerce, India

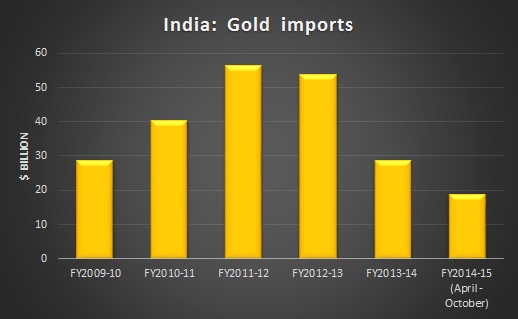

Source - Ministry of Commerce, IndiaGJF has also urged the government to provide incentives in the jewellery manufacturing sector and reintroduce metal gold loans (MGL) with lower interest rates to promote manufacturing in the sector in India. It has also asked the government to exclude jewellery from all bilateral or multi-lateral free trade agreements (FTAs), develop skill upgradation programmes in the sector ease rules for transport and manufacturing, and develop a comprehensive gold mining policy in India. India is the world’s largest importer of gold, accounting for around 20% of global gold imports and around 6% of India’s overall imports. India’s gold imports during April – October 2014 stood at around $18.8 billion, according to the Ministry of Commerce, India. Recently, a report by the Federation of Indian Chambers of Commerce and Industry (FICCI) and the World Gold Council (WGC) said that India, as a top importer and consumer of gold, should frame a Gold Policy to manage imports, encourage exports and facilitate development of the infrastructure needed to ensure the Indian gold market functions to maximum effect. The report also said that India needs to improve its marketing strategy for Indian handcrafted jewellery. “This could boost exports and highlight India’s expertise in this highly-valued sector e.g. by promoting handcrafted ‘India-made jewellery’ like the Swiss-made watches,” it said.

This article was published on January 17, 2015.

to success.

to success.